Natural Monopoly – Regulation and Subsidy

Microeconomics

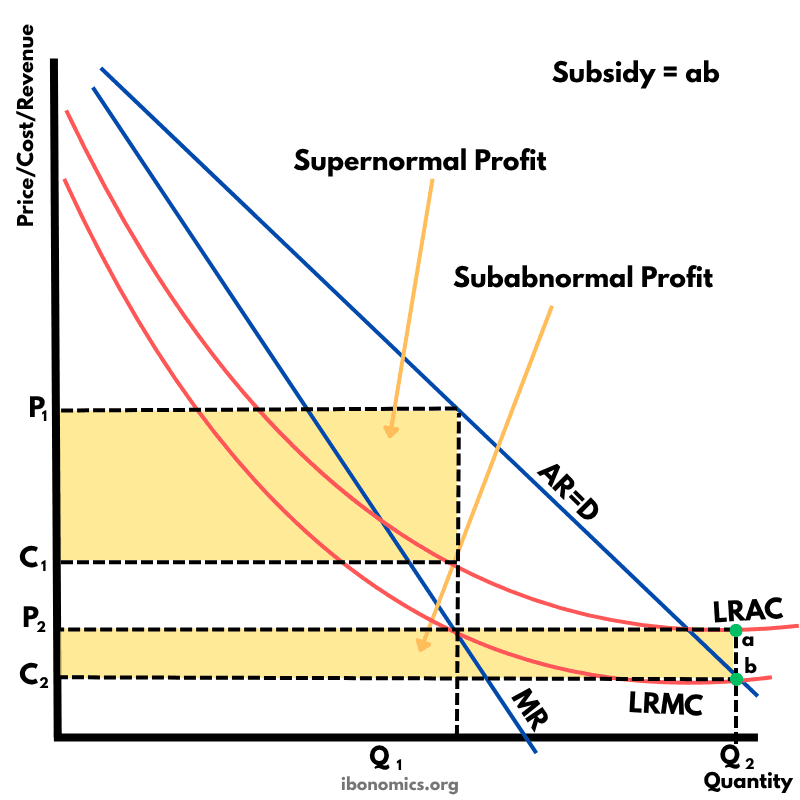

A diagram illustrating a natural monopoly regulated to achieve allocative efficiency through subsidies. It highlights supernormal and subabnormal profit regions, along with the required subsidy to sustain production at the socially optimal quantity.

Curves and Elements

ar

AR = D: The average revenue or demand curve, downward sloping.

mr

MR: Marginal revenue curve, lies below AR due to price reduction on all units.

lrac

LRAC: Long-run average cost, continuously decreasing due to economies of scale.

lrmc

LRMC: Long-run marginal cost, intersects MR at the profit-maximizing quantity.

q1

Q1: Profit-maximizing output where MR = LRMC, yielding supernormal profit.

p1

P1: Price charged at Q1, generating supernormal profit (area between P1 and C1).

c1

C1: Cost per unit at Q1, based on LRAC.

q2

Q2: Allocatively efficient output where AR = LRMC.

p2

P2: Price consumers pay at Q2 under government regulation.

c2

C2: Cost per unit at Q2, above the price, resulting in subnormal profit.

subsidy

ab: Vertical distance representing the per-unit subsidy needed to cover the loss at Q2.

A natural monopoly arises when one firm can supply the entire market at a lower cost than multiple firms due to large economies of scale.

At Q1, the firm maximizes profit where marginal revenue (MR) intersects long-run marginal cost (LRMC), charging price P1 and enjoying supernormal profit (shaded area between P1 and C1).

Allocative efficiency occurs at Q2, where the price (P2) equals LRMC, but at this point, the firm incurs a subnormal profit since cost C2 exceeds price P2.

To sustain production at Q2, the government provides a subsidy equal to the vertical distance ab — the loss per unit that the firm would incur at the allocatively efficient level.

This type of regulation improves societal welfare by increasing output and lowering prices, despite requiring taxpayer funding to cover the firm's losses.

More Microeconomics Diagrams

Explore other diagrams from the same unit to deepen your understanding

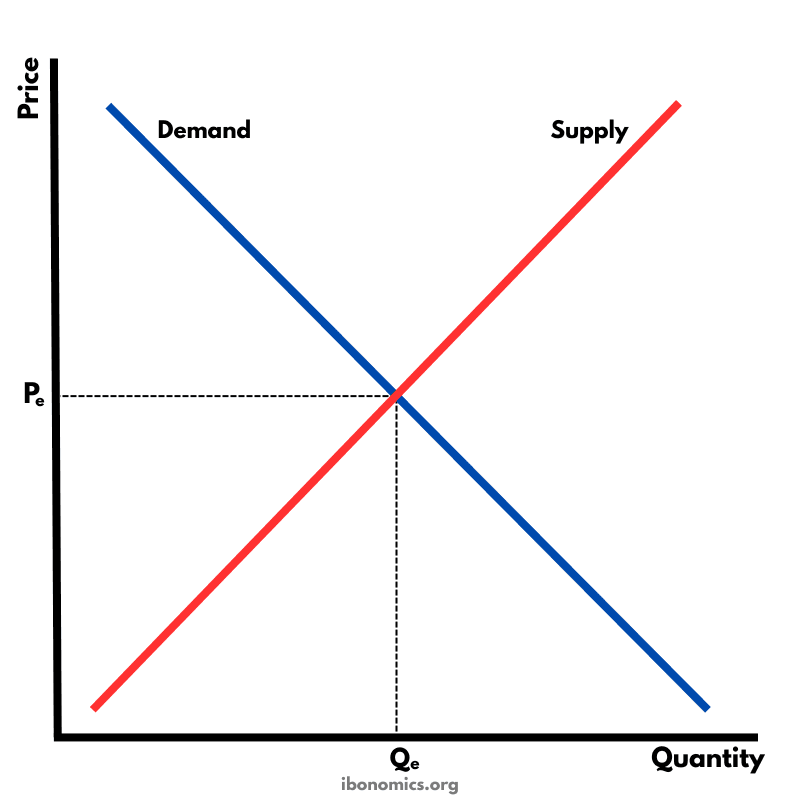

The fundamental diagram showing the relationship between demand and supply in a competitive market, determining equilibrium price and quantity.

A basic diagram showing the inverse relationship between price and quantity demanded, illustrating the law of demand.

A basic diagram showing the positive relationship between price and quantity supplied, illustrating the law of supply.

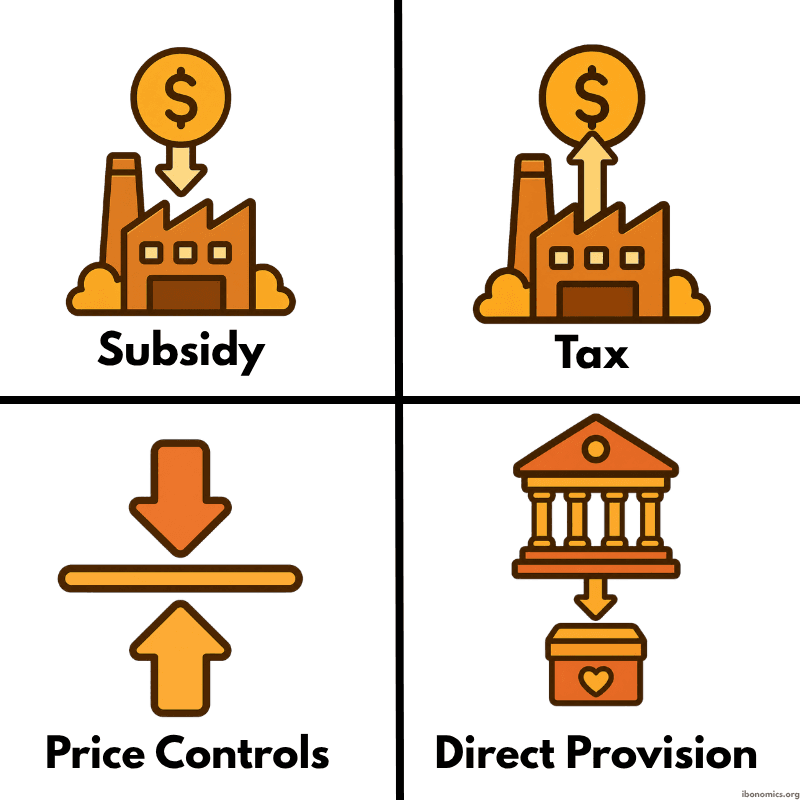

A simple diagram showing four common forms of government intervention in markets: subsidies, taxes, price controls, and direct provision.

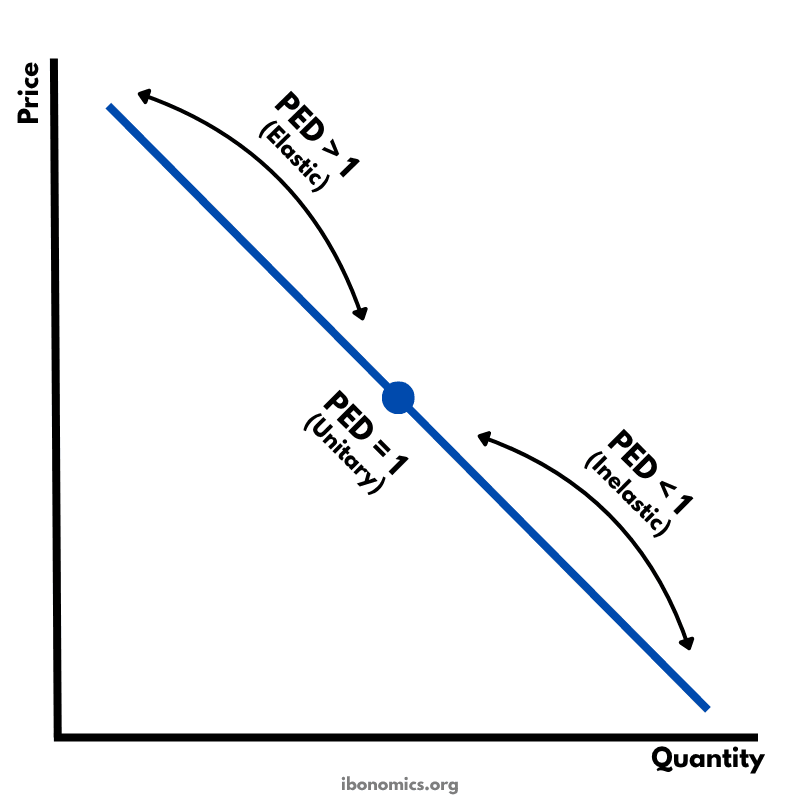

A diagram showing how price elasticity of demand changes along a straight-line demand curve, from elastic to unitary elastic to inelastic.

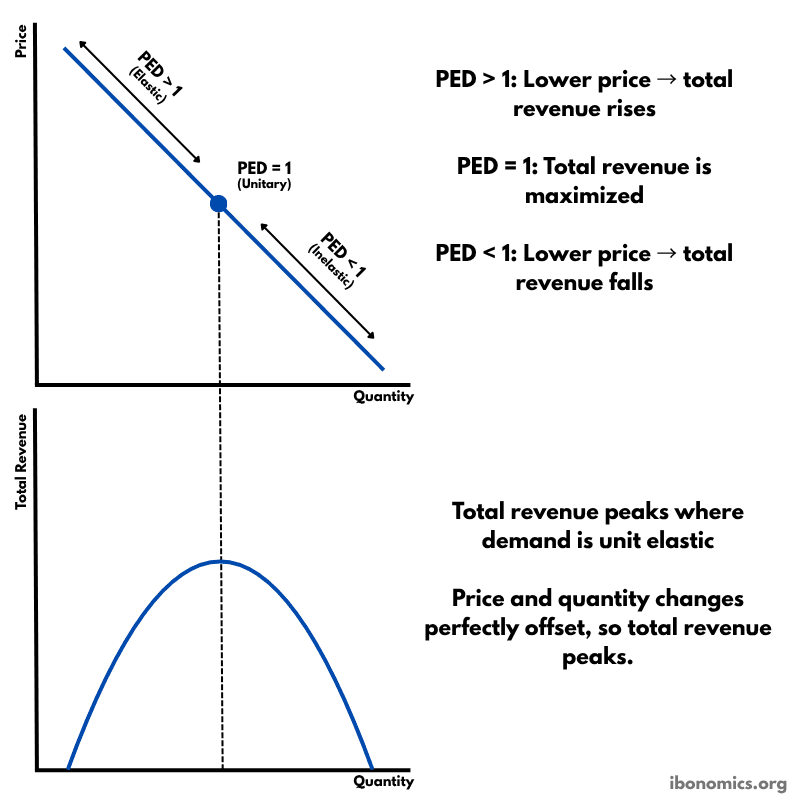

A diagram showing how price elasticity of demand affects total revenue, with total revenue maximized where demand is unitary elastic.