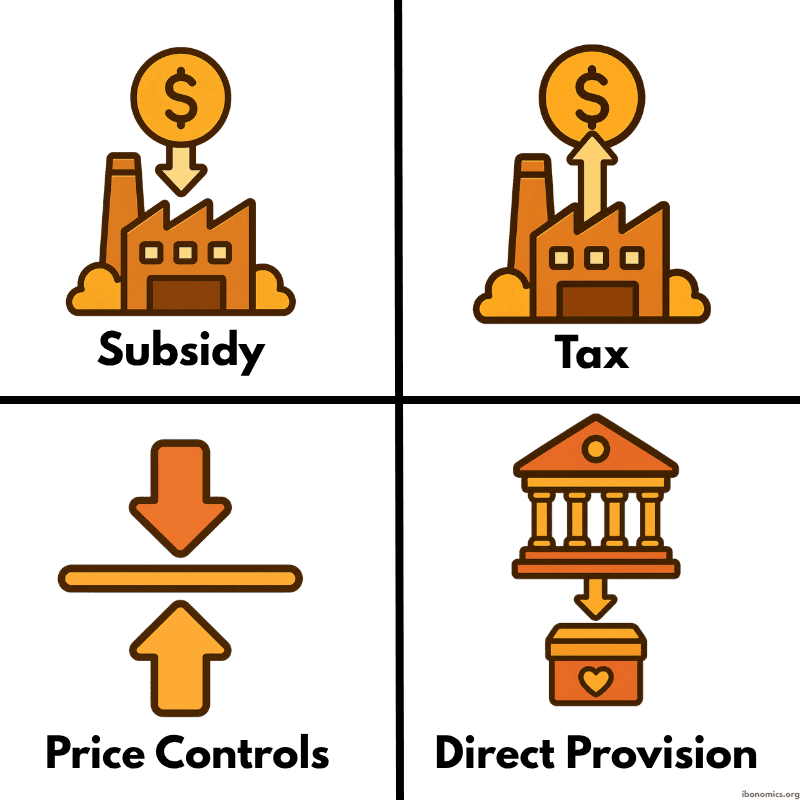

Forms of Government Intervention

Microeconomics

A simple diagram showing four common forms of government intervention in markets: subsidies, taxes, price controls, and direct provision.

Curves and Elements

subsidy

Subsidy: Government financial support that lowers costs of production or consumption and encourages market activity.

tax

Tax: Government charge placed on producers or consumers that raises costs and discourages market activity.

price controls

Price Controls: Government intervention through maximum or minimum prices to influence market outcomes.

direct provision

Direct Provision: The government supplies a good or service itself rather than leaving it fully to the private market.

A subsidy is financial support given by the government to producers or consumers to encourage production or consumption.

A tax is a charge imposed by the government, which increases costs and can reduce production or consumption.

Price controls are government-set minimum or maximum prices, such as price floors and price ceilings.

Direct provision occurs when the government provides goods or services itself, often to improve access and equity.

More Microeconomics Diagrams

Explore other diagrams from the same unit to deepen your understanding

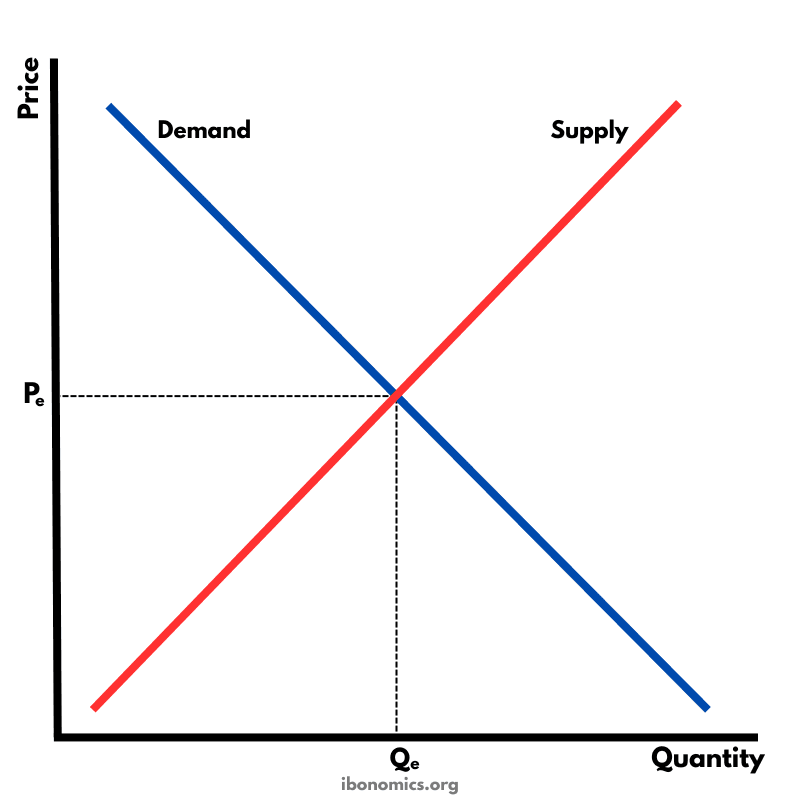

The fundamental diagram showing the relationship between demand and supply in a competitive market, determining equilibrium price and quantity.

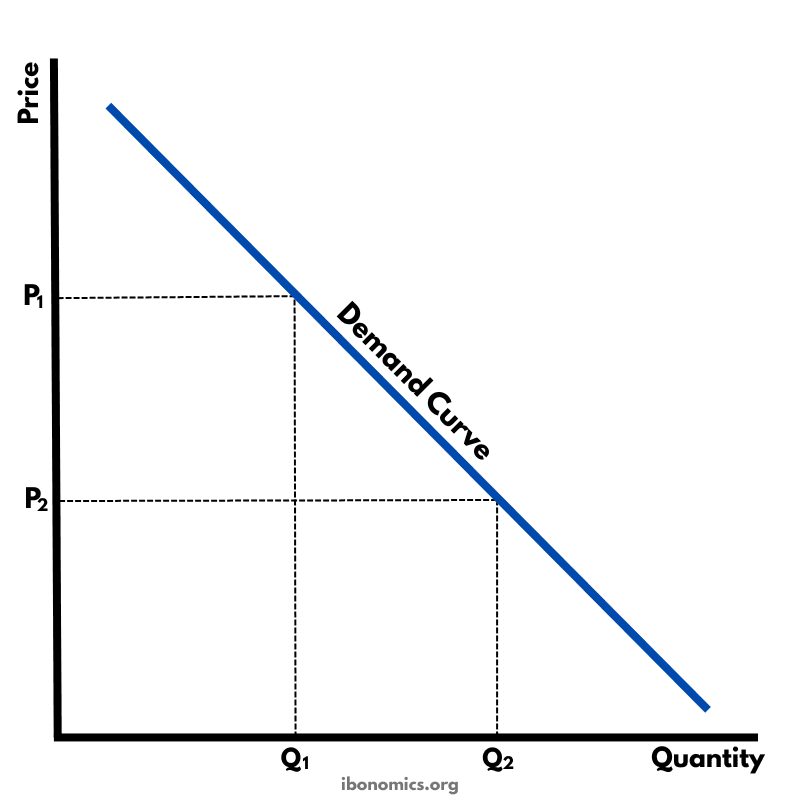

A basic diagram showing the inverse relationship between price and quantity demanded, illustrating the law of demand.

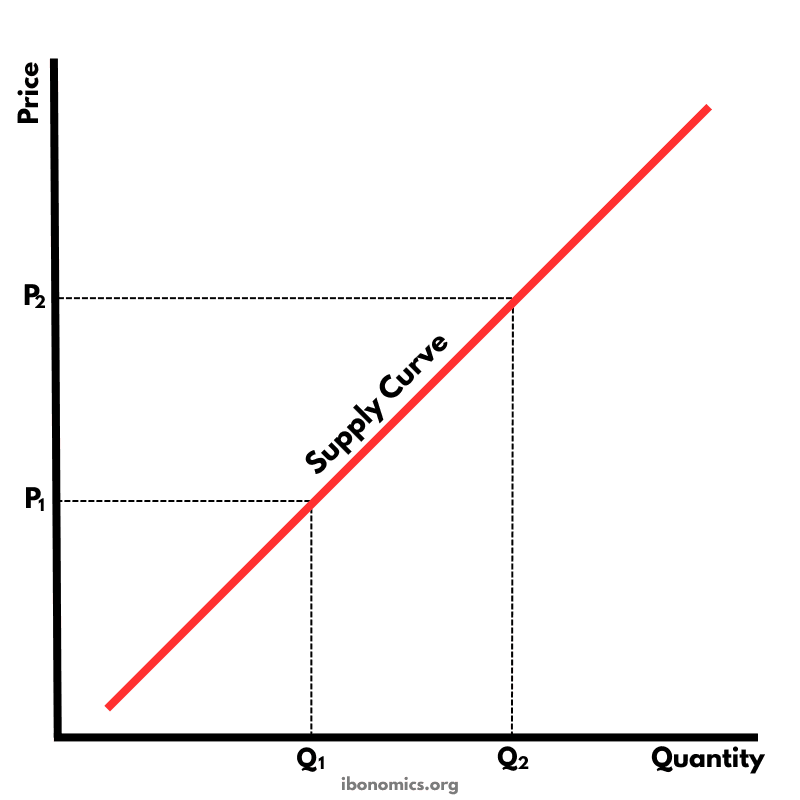

A basic diagram showing the positive relationship between price and quantity supplied, illustrating the law of supply.

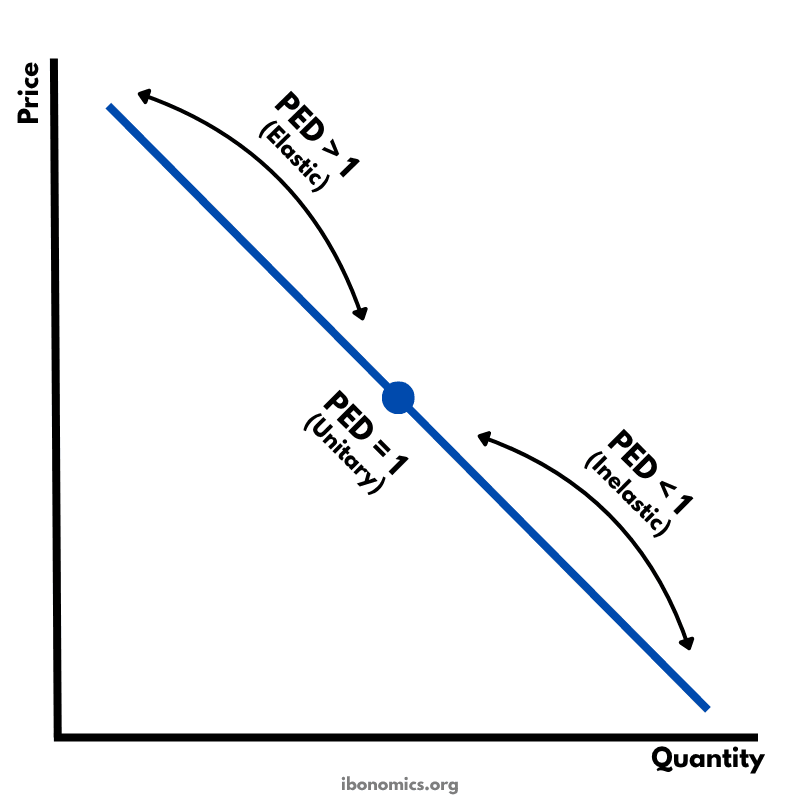

A diagram showing how price elasticity of demand changes along a straight-line demand curve, from elastic to unitary elastic to inelastic.

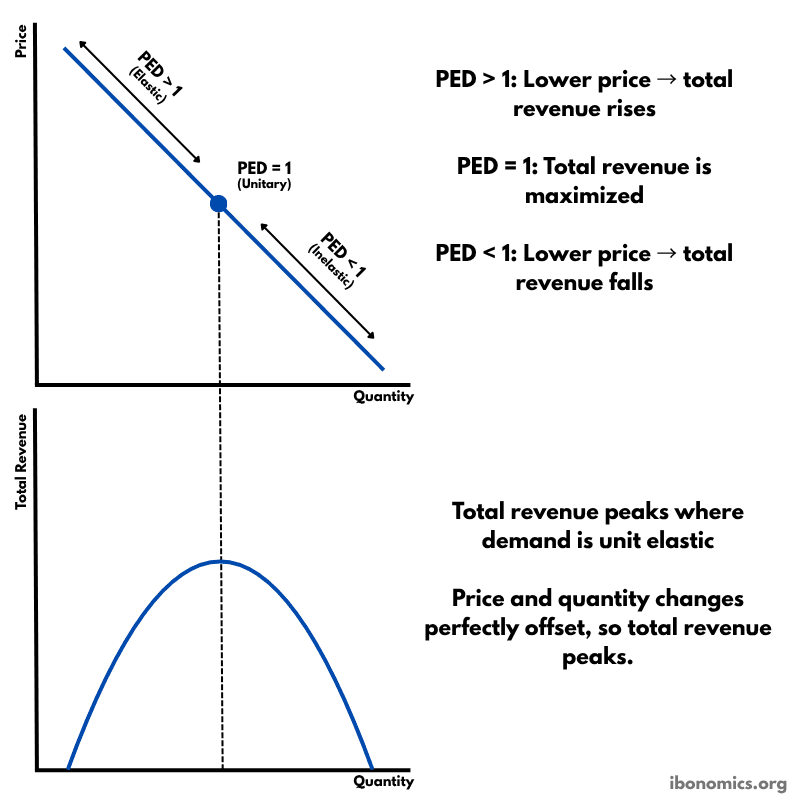

A diagram showing how price elasticity of demand affects total revenue, with total revenue maximized where demand is unitary elastic.

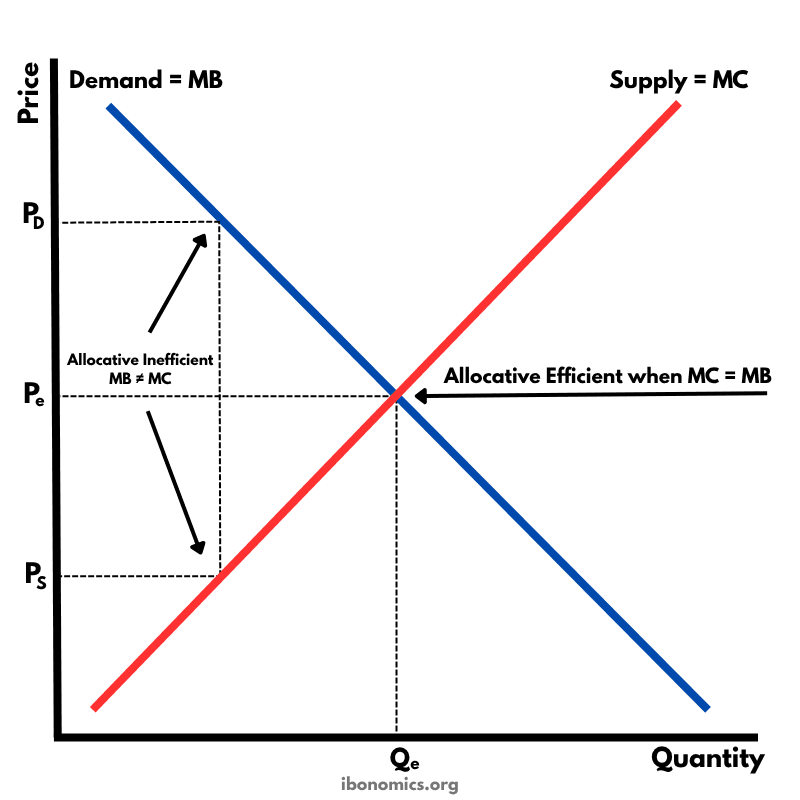

A diagram showing that allocative efficiency occurs where marginal benefit equals marginal cost, meaning resources are allocated to maximize welfare.