Rethinking Monetary Policy in IB Economics: From Money Supply to Interest-Rate Rules

Why the IB Economics syllabus should move away from money-supply stories and instead teach how modern central banks set policy interest rates using rules like the Taylor rule, and what this means for SL and HL students in an age of AI-powered learning.

Rethinking Monetary Policy in IB Economics

Many IB Economics students still learn monetary policy using a story that feels increasingly disconnected from how real central banks work. The usual explanation is that the central bank changes the money supply in the economy, and that the money market then determines the interest rate. In practice, modern central banks like the European Central Bank (ECB) and the Federal Reserve directly set a short-term policy interest rate and adjust the supply of money and bank reserves to support that rate.

This article argues that the IB Economics syllabus should gradually shift its focus. Monetary policy should be taught as “the central bank chooses an interest rate according to some rule, which then shifts aggregate demand (AD)” rather than “the central bank changes the money supply to move the interest rate.” The change would better match current macroeconomic research, real-world policy practice and the learning possibilities created by AI-based study tools.

The Traditional IB Story: Money Supply and the Interest Rate

In many IB courses, students encounter monetary policy through a money market diagram. The central bank is shown as fixing the quantity of money, which appears as a vertical money-supply curve. Money demand slopes downward with respect to the interest rate, and the intersection of money supply and money demand sets the nominal interest rate.

This story is linked to the older IS–LM model. The IS curve shows combinations of national income and interest rates where the goods market is in equilibrium. The LM curve summarises combinations of national income and the interest rate that clear the money market. Lowering the interest rate involves shifting the money-supply curve to the right, which moves the LM curve and ultimately shifts the aggregate demand curve in the AD–AS diagram.

Historically this approach reflected a time when some central banks tried to target the growth of the money supply directly. But over the past few decades most major central banks have moved away from monetary-aggregate targets. Today they primarily target short-term interest rates and use money and reserves as tools, not as the main policy objective.

How Central Banks Actually Set Policy Today

Modern central banks operate with an explicit interest-rate target. The ECB talks about setting “key interest rates” to steer borrowing costs in the euro area and keep inflation close to its target. The Federal Reserve describes its framework as one in which it supplies plenty of bank reserves and uses the interest rate it pays on those reserves as the main tool for controlling short-term market interest rates.

In plain language, central banks choose a short-term policy interest rate and then do whatever is needed in money and bond markets to keep actual market rates close to that chosen level. The quantity of reserves and base money is largely a side effect of these decisions, not the number that is fixed first.

For IB students, it makes more sense to see monetary policy as a story about how central banks choose interest rates and how those choices affect aggregate demand and inflation, instead of a story about a fixed money supply determining interest rates in a simple money market.

The Shift in Macroeconomics: From IS–LM to IS–MP

Macroeconomics as a discipline has already responded to this change. A well-known step in this direction was an article titled “Keynesian Macroeconomics Without the LM Curve,” which argued that the standard IS–LM–AS model was no longer the best baseline for teaching short-run fluctuations. The idea was to replace the assumption that the central bank targets the money supply with an assumption that it follows a simple interest-rate rule.

In this newer framework, instead of an LM curve, we use an MP curve. MP stands for “monetary policy.” The MP curve shows how the central bank sets the real interest rate given inflation and output. One common way to describe the MP curve is through the Taylor rule.

The Taylor rule is a guiding formula that says the central bank should raise the interest rate when inflation is above its target or when output is above its long-run level, and should cut the interest rate when the opposite is true. In simple terms, the rule says “if inflation is too high, raise the rate; if inflation is too low, cut the rate; if output is weak, loosen policy; if output is strong, tighten policy.”

Different textbooks and teaching resources have started to adopt this IS–MP approach, especially at introductory level. It better reflects both modern theory and how central banks actually communicate their decisions. Press conferences and policy reports nearly always speak in terms of interest rates, inflation targets and output gaps, not in terms of a fixed money supply.

Reinterpreting IB Diagrams: Central Banks as Interest-Rate Setters

None of this means that IB students have to abandon familiar diagrams. It mainly means reinterpreting them.

First, consider the IS curve. The IS curve shows combinations of real interest rates and output where planned spending equals actual output. When the interest rate falls, investment and consumption tend to rise, so output increases and the economy moves along the IS curve.

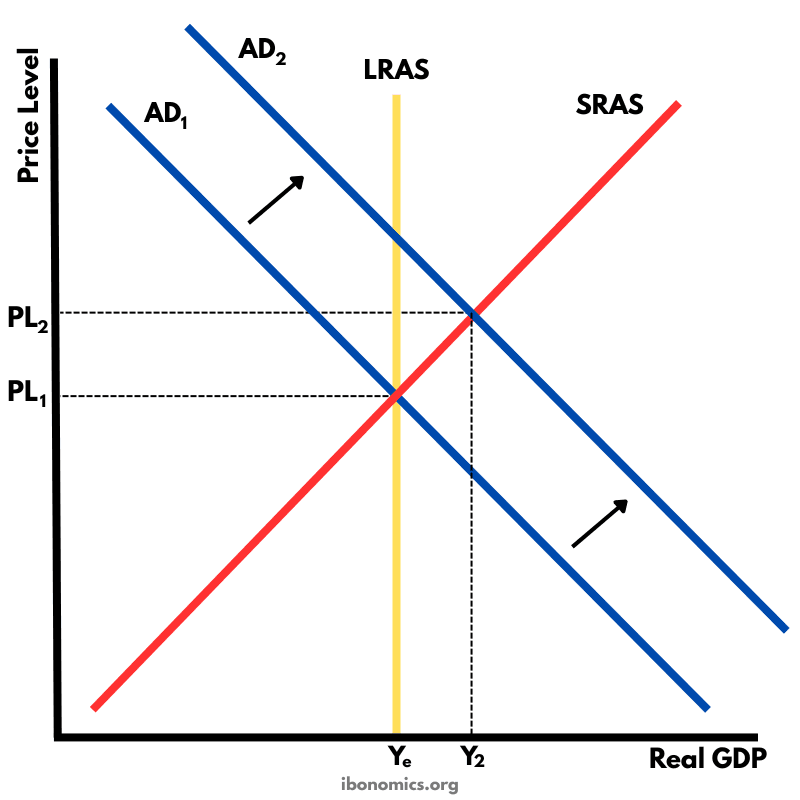

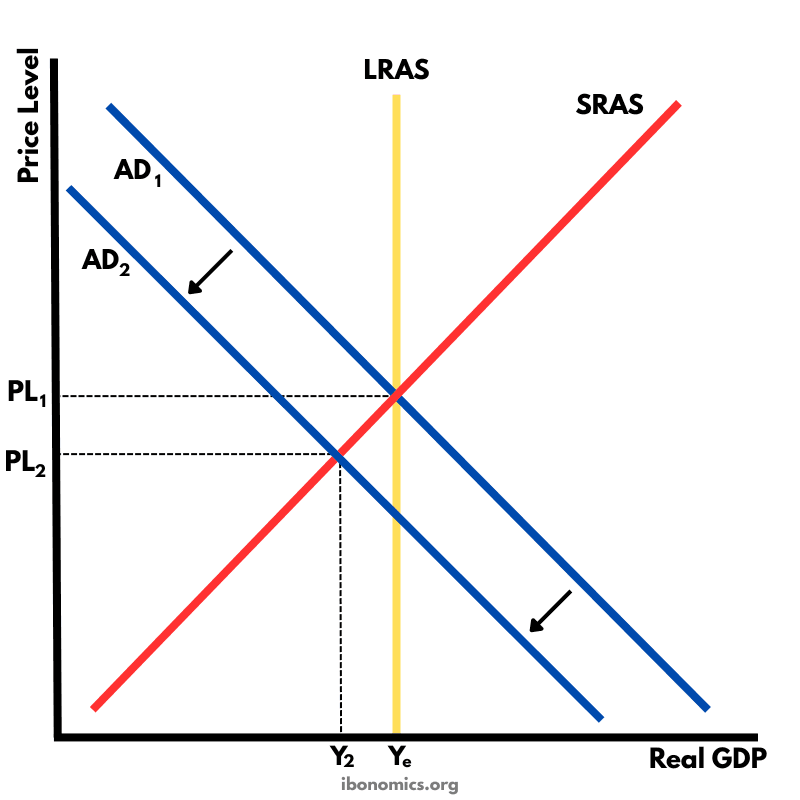

Next, think about the aggregate demand curve. The AD curve can be seen as the result of combining the IS relationship with the way the central bank sets the interest rate. When the central bank cuts its policy rate, the real interest rate falls, demand for goods and services rises, and the AD curve shifts to the right in the AD–AS diagram.

If we treat the central bank as the direct chooser of the interest rate, we can replace the old “money market determines the interest rate” story with a simpler and more realistic one. Students can learn that the central bank chooses a policy interest rate, often using a rule that responds to inflation and economic activity. This interest rate affects spending through the IS curve. The changes in spending shift the AD curve and therefore influence real output and inflation in the short run.

Money supply and reserves still play a role, but mainly in the background as part of the operating framework that allows the central bank to keep market rates close to its chosen policy rate. For most IB questions this level of detail is not necessary, and the interest-rate story is enough to capture the main ideas.

How the IB Syllabus Could Integrate the Taylor Rule

At Standard Level (SL), IB Economics could make a modest shift by changing the language used to describe monetary policy. Instead of saying that the central bank “increases the money supply” to lower interest rates, textbooks and teachers could say that the central bank “lowers the policy interest rate,” and then briefly explain that it adjusts its operations to achieve that rate. The underlying message would become “the central bank targets the interest rate, not the quantity of money.”

At Higher Level (HL), there is room for a slightly more formal treatment. The syllabus could introduce a very simple version of the Taylor rule.

A possible HL explanation could be:

The Taylor rule is a basic guideline for interest-rate decisions. It says the central bank should set the interest rate higher when inflation is above the inflation target or when the economy is producing above its normal level, and lower when inflation is below target or when the economy is weak.

HL students could see a simple MP curve that is upward sloping in a graph with inflation on the horizontal axis and the real interest rate on the vertical axis. A higher inflation rate leads to a higher policy interest rate according to the rule. Students could then analyse how different shocks, such as an oil price increase or a fall in investment confidence, move the IS curve, interact with the MP curve and finally affect the AD–AS diagram.

This would give HL students a clearer link between theory, diagrams and real central-bank communications that regularly reference inflation targets, expected future interest rates and assessments of economic slack.

AI, Learning and the Need for Deeper Monetary-Policy Questions

The rise of artificial intelligence in education is already changing how students practise and revise. It is now easy to generate large numbers of routine questions about simple money-supply and money-demand diagrams or basic shifts in AD and AS. Students can drill these questions until they become mechanical.

As AI-based quiz production becomes more common, there is a real possibility that the average student’s ability to handle routine questions will rise. If the syllabus and exams do not adapt, simple diagram-based questions could become too easy and less effective at sorting different levels of understanding.

One response is to increase the conceptual difficulty of monetary-policy questions. Instead of asking only “what happens to the money market when the central bank increases the money supply,” exams could focus more on questions like:

Why might a central bank keep interest rates unchanged even when inflation is above target?

How does an unexpected inflation shock affect an economy where the central bank follows a Taylor-type rule?

What are the short-run and medium-run effects of a systematic, rule-based tightening of monetary policy compared with a one-time surprise increase in the interest rate?

These kinds of questions require students to connect models with reasoning and real-world policy, which is much harder for AI tools to answer on behalf of a specific student in an exam setting. In class and at home, students can still use AI-generated quizzes to build basic skills, but the exam system would reward understanding, explanation and evaluation.

A Practical Roadmap for Updating IB Monetary Policy

A realistic update to the IB Economics syllabus does not require a complete overhaul. It can be done in gradual steps that build on what is already taught.

First, the language of monetary policy should be updated so that the central bank is presented as an interest-rate setter. The money-supply story can be explained as a useful simplified model of the past, but not as the core description of current practice.

Second, the syllabus can introduce the idea of a monetary policy rule. At SL, this can remain verbal and intuitive: “central banks raise rates when inflation is too high and cut them when it is too low.” At HL, a basic Taylor rule and MP curve can be shown without heavy mathematics, just enough to support diagram analysis and evaluation.

Third, exam and IA prompts can be redesigned to reflect this approach. Students could be asked to read short extracts from central-bank reports, identify the policy stance, and explain how it fits with an interest-rate rule. They could be asked to use IS, MP and AD–AS diagrams together to analyse a shock(although this can easily get too complicate for many). This would encourage them to think about policy as it is actually discussed in the news and in central-bank communication.

Conclusion: Aligning IB Economics with Modern Monetary Policy

The gap between the traditional IB story of monetary policy and actual central-bank practice has widened over time. Central banks no longer see themselves as setting the money supply and waiting for the money market to determine the interest rate. They choose interest rates directly, often following rule-like behaviour that responds to inflation and output. Money and reserves adjust in the background.

By updating the syllabus to emphasise interest-rate rules, IS–MP style thinking and the way monetary policy shifts aggregate demand, IB Economics can remain relevant, rigorous and realistic. Such a shift would also make better use of AI-driven learning tools, which are best at drilling routine skills, by pushing classroom teaching and assessment towards deeper understanding, evaluation and real-world application.

For students, this change would mean a more accurate picture of how modern economies are managed. For teachers, it would provide clearer links between diagrams, theory and the language of central banks. And for the IB programme as a whole, it would strengthen the claim that its graduates are ready to think carefully about the macroeconomic challenges facing the world today.

Related syllabus topics

Demand Management (Monetary Policy)

Unit 3.5: Demand Management (Monetary Policy)

Monetary Policy Introduction

Unit 3.5: Demand Management (Monetary Policy)

Goals of Monetary Policy

Unit 3.5: Demand Management (Monetary Policy)

Monetary Policy Tools (HL only)

Unit 3.5: Demand Management (Monetary Policy)

Money Market and Interest Rates (HL only)

Unit 3.5: Demand Management (Monetary Policy)

Real vs Nominal Interest Rates

Unit 3.5: Demand Management (Monetary Policy)

Expansionary and Contractionary Monetary Policy

Unit 3.5: Demand Management (Monetary Policy)

Effectiveness of Monetary Policy

Unit 3.5: Demand Management (Monetary Policy)